Non-Residential Building Spending Projected to Decline Through 2021, Says AIA

The AIA's July 2020 Consensus Construction Forecast; click to view in greater detail. Image courtesy AIA.

The AIA released a mid-year update to its Consensus Construction Forecast on July 21, 2020. Read the update, by AIA Chief Economist Kermit Baker, below.

Commercial buildings slated to see the bulk of the downturn; slowdown for institutional facilities predicted to be relatively modest

The construction sector appears to be faring during the pandemic more robustly than, for example, travel, hospitality, and most other service sectors that rely on face-to-face interaction. However, construction has not been able to altogether avoid the economy-wide decline. With so much of the economy in slowdown or shutdown mode, businesses and organizations are hesitant to invest in modernized or new facilities. As a result, construction spending ended its almost decade-long expansion this past spring, and it appears that it will remain in recession throughout 2020 and well into 2021.

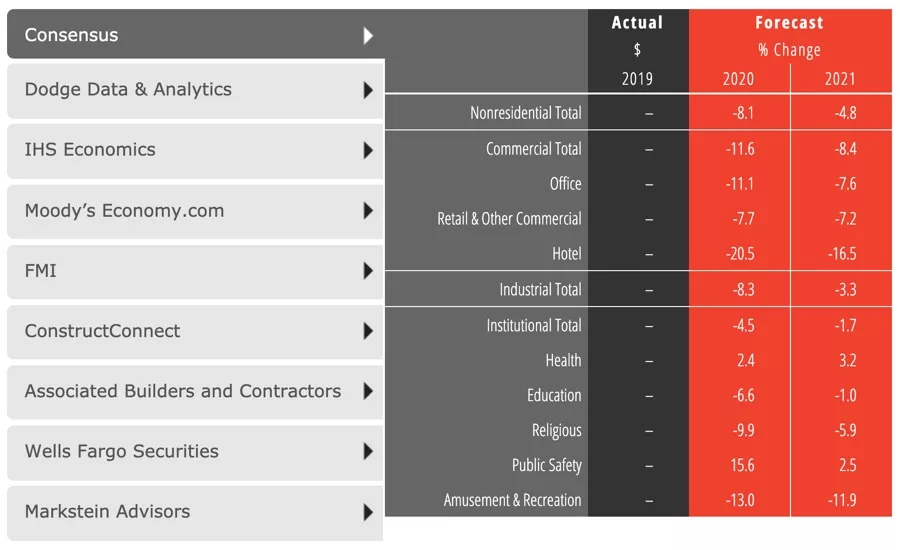

Spending on nonresidential facilities will decline just over 8% this year, and another 5% next year, according to The American Institute of Architect’s recently released mid-year update to its Consensus Construction Forecast. The commercial building sector (office, retail and other commercial structures, and hotels) is expected to be the hardest hit, with spending projected to decline almost 12% this year and an additional 8% in 2021. The industrial sector (manufacturing production and related distribution facilities) is slated to see declines of 5% this year and 3% in 2021 . While institutional buildings (health care, education, religious, public safety, and amusement and recreation) will fare the best on the nonresidential side, spending on these facilities is projected to drop almost 5% this year, and another 2% next year.

Economic recovery stalling

As much of the economy shut down in mid-March to help limit the spread of COVID-19, there was hope that after the initial steep decline in economic activity there could be an almost equally quick recovery. Both monetary (reduction in interest rates and aggressive lending by the Fed) and fiscal policy (in total, almost $3 trillion in federal stimulus) were designed to keep households and small businesses afloat until the economy could generate a sustainable recovery.

With almost 50 million individuals applying for unemployment insurance benefits since mid-March, and five million small businesses receiving over $500 billion in loans through the Small Business Administration’s Payroll Protection Program, there was hope that this stimulus strategy was poised for success. The May and June payroll reports indicated that the economy added 7.5 million net new jobs, after shedding 22 million in March and April. The national unemployment rate fell from 14.7% in April to 11.1% in June. As a result, consumer sentiment and consumer expectation scores rose in May and June after dropping dramatically in March and April.

However, since mid-June, economic growth has stalled. This timing coincides with a spike in new COVID-19 cases across the country, and the pausing or rolling back of reopening plans in many states. Unfortunately, the slowing or even potential reversal of the recent modest economic rebound is coming just as the supplemental federal employment insurance payments and the required expenditure of the PPP loans are nearing their expiration. As such, it is extremely unlikely that the economy can support self-sustaining growth anytime soon.

Still, economic conditions have been in a constant state of flux since the pandemic hit, and there is no reason to think that the volatility won’t continue. As of now, the upside risks are that economic conditions could improve more than expected, and the downside risks are that they could deteriorate more that than expected are just about balanced. Upside risks at present include: the potential for further fiscal stimulus; a strengthening housing market; a possible early vaccine; stronger than expected international growth; and necessary facility retrofits.

Looking for quick answers on architecture and design topics?

Try Ask RECORD, our new smart AI search tool.

Ask RECORD →

Potential additional stimulus – The expanded unemployment insurance and small business loans under the PPP have helped stabilize economic conditions. With both set to expire, extending these programs could further backstop a more severe downturn. Additionally, support for state and local government and an infrastructure program would be beneficial to boost the economy.

A strengthening housing market – Increases in purchase mortgage applications, growth in residential building permits, firming in the existing homes sales market, and gains in homebuilder confidence all point to growth in the housing sector. Housing is not only a leading indicator for the economy, but generally foreshadows movement in the broader construction sector.

Possible early vaccine – A COVID-19 vaccine is generally expected to be available around the middle of 2021. However, all the current research could yield results by late 2020 or early 2021, which would be a tremendous boost to accelerating the economic expansion.

Stronger international growth – The international economy is not expected to do significantly better than the U.S. economy this year and next. However, the Chinese economy may well see growth in 2020, and India is projected to significantly outperform the U.S. in coming years, both which would produce export opportunities for U.S companies. Unfortunately, two of our biggest trading partners, Canada and Mexico, are seeing economic declines on par with or greater than the U.S.

Facility retrofits – Once the economy reopens, there will be a dramatic need for post-pandemic design in most existing buildings. This will drive a surge in building retrofits, which will benefit the design and construction industries.

However, there are also a set of downside risks that could further delay a stronger economic recovery: a much longer timeline to bring the pandemic under control; the need for new business models; growing evictions/defaults/bankruptcies feeding into a more traditional demand-driven recession; and growing trade tensions.

Resurgence of pandemic concerns – While there was optimism that the pandemic was beginning to wane, beginning around mid-June infection rates began to accelerate, particularly in states that had performed fairly well in the early months. Many of these states are pausing or even reversing their re-opening plans, which will delay economic growth. Additionally, there is growing concern that a second round of COVID-19 infections will re-emerge in the fall.

New business models – Even in those areas where businesses are successfully re-opening, the realities of running a profitable business in a post-pandemic economic environment can be daunting. An airline or restaurant that is allowed to operate at only 40% or 50% of its former capacity will obviously struggle to remain viable, and these constraints may be in place for an extended period of time.

Household and business financial pressures – The longer the economic slowdown continues, the less likely it is that households and business will have the financial ability to ultimately withstand the downturn. For example, to date most renters and homeowners have been able to make their monthly rent and mortgage payments. However, in the absence of further government support, the more this situation is likely to spiral out of control. If this situation continues to cycle down, it will manifest itself in growing evictions, mortgage defaults, and ultimately, business failures.

Emerging trade tensions – As countries vie for shrinking trade opportunities, there is a growing likelihood that governments will use tariffs to protect their domestic industries. This has the potential to boil up into a trade war.

Commercial sector bears the brunt of the weakness

While virtually all major construction sectors are expected to see declines this year and next, the expected declines are generally greatest in the commercial categories. Even entering 2020, the commercial sector was expected to be weak, and the pandemic has only exacerbated this situation.

Offices – The dramatic downturn in office employment will limit the need for new facilities. Additionally, though, many businesses have found telecommuting to be an attractive option, and many workers feel safer at home, particularly those relying on public transportation for their work commute. Others don’t mind avoiding their commute, even in the safety of their car. Spending on office construction is expected to decline 11% this year, and almost 8% next.

Retail – Shopping habits were changing even before the pandemic, and the growing list of recent retail bankruptcies demonstrates that many of these companies were on the verge before the pandemic. Online shopping clearly picked up dramatically in recent months, and many are now turning more frequently to the convenience of shopping from home. Spending on retail facilities is expected to continue its 2019 weakness, declining 8% this year and 7% next.

Hotel – The hotel construction sector is expected to be the weakest major nonresidential sector, declining over 20% this year and another almost 17% in 2021. While competition from Airbnb and other online sources were already limiting the need for new hotels, the pandemic has accelerated this weakness. Personal travel has seen a steep decline, but business travel has grown even weaker. The conversion of most conventions and trade shows to virtual events has had a dramatic effect on hotel demand.

Institutional construction is also projected to pull back this year and next, although much less significantly than for the commercial sector. Institutional building relies more heavily on public and nonprofit funding, and given that the stock market is holding up reasonably well, endowments may not be hit as hard as previously feared.

Health care – Health care construction is one of the few sectors expected to avoid a recession this cycle. Even though elective health treatments have fallen off in recent months, demographics remain very positive for health care spending moving forward. One wild card is the long-term trend toward telemedicine, and whether that will continue to be a popular alternative to in-person care. Health care spending is projected to increase over 2% this year and another 3% next.

Education – At almost $100 billion in spending last year, education is the largest nonresidential building category. Spending on education facilities saw a modest gain last year, but is projected to decline almost 7% this year, and another 1% next. With many schools and colleges relying heavily on virtual teaching for the remainder of 2020, there is less need for additional facilities, and fewer resources to support them. Additionally, the demographics supporting growth in educational facilities are mixed, with slower growth for college age students leading to a modest net decline in college enrollments in recent years.

After almost a decade of steady growth, the nonresidential construction cycle was losing steam heading into this pandemic-induced recession. In all likelihood, this construction downturn will be shorter, and result in less of a spending decline that the 33% falloff during the Great Recession. However, economic conditions have been extremely fluid recently, so the future path remains uncertain.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!