Architects Hit Hard by Financial Crisis

The plunging financial markets this month, followed by unprecedented responses from the federal government, have left many Americans bracing for a deep recession. In the architecture profession, however, the downturn has already arrived, according to a key measure of the market for architectural services.

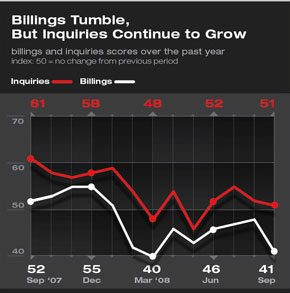

As of August, the Architecture Billings Index (ABI), which the American Institute of Architects compiles in part from statistics provided by firms, had dipped below 50 for seven straight months, hitting 39.7 in March, the lowest score in the index’s 13-year history. Anything below 50 represents a billings decrease. In contrast, the score rose above 50 every month last year; in fact, prior to 2008, the score had dropped below 50 on only one occasion (June 2006) in the past three years.

Next year looks even more dismal, according to a July report from the AIA’s Consensus Construction Forecast Panel, which predicts retail and hotel building will fall 10 percent in 2009 while office construction plummets 12 percent. Anticipating the slowdown, the AIA recently established an online resource center to help architects weather these tough times.

The credit crunch has plagued every sector, particularly the commercial sector. While FDIC records don’t yet show measurable reductions in construction lending through June, anecdotal evidence suggests fewer loans are being issued. Major banks like Citi and Chase have gradually closed the taps, while other lenders have vanished altogether, like Lehman Brothers, which filed for bankruptcy protection in September.

Smaller regional banks, which tend to be less leveraged, still seem to be lending money for development projects, especially if the project is non-speculative. And the tumbling stock market might actually increase some capital reserves, according to bank officials. “Deposits are up, because of a flight to safety, and my bankers are looking for someplace to invest them,” says Joe DeHaven, president of the Indiana Bankers Association.

Still, fundamental problems pose long-term challenges for the commercial sector, says Kermit Baker, AIA chief economist. Shrinking payrolls means there’s less need for new office space. And in terms of retail, if people cut back on shopping, why build stores? Plus, material prices for concrete, copper, and asphalt continue to be steep, making construction an increasingly pricey proposition. “There is just less willingness to assume risk in this environment,” Baker says, noting that it doesn’t matter if a project is pre-leased, or guaranteed to be 100-percent occupied.

The housing sector also is limping, as depressed home values are turning off developers, and buyers are struggling to secure mortgages. In August, the ABI’s multi-family housing score was 40.8, well below 50, though up from its March low of 31.7. While the ABI doesn’t measure the single-family housing sector, its numbers also are down. According to the AIA’s second quarter Home Design Trends Survey, released in September, billings and inquiries for residential projects hit their lowest levels (38 and 37, respectively) in the survey’s three-and-a-half year history.

William Gati, AIA, principal of Architecture Studio, based in Queens, New York, says the demand for the $3 million luxury homes he was building four years ago is off by 60 percent. He expects his practice to persevere because he’s socked away money for rainy days. “But firms that are going into business now,” he says, “will be out of business soon.”

A bright spot in the ABI this year has been the institutional sector, which has produced 50 or better ratings for 44 straight months. But even that sector is now vulnerable.

Gerald Reifert, AIA, is a managing partner at Seattle-based Mahlum Architects, a 95-member firm that focuses almost exclusively on the institutional sector. His recent projects include University of Washington dorms and two new hospitals. While he remains optimistic, these types of projects typically require bond financing, and thus voter support, and “people are nervous right now about money,” he says. In fact, lack of financing for new schools in nearby Portland, Oregon, where he has an office, has forced him to relocate some of his Portland employees to Seattle.

For public projects, taxpayer money isn’t the only funding source jeopardized by the economic downturn. School endowments, which typically are invested in the stock market, can take a hit, says Rebekah Gladson, AIA, campus architect at the University of California, Irvine.

Gladson, who’s been practicing for three decades, sees a difference between this downturn and the early-1990s version. As she explains, materials, despite a drop in demand, continue to be expensive, largely because of overseas orders from Dubai, Shanghai, and Beijing. That market globalization does have upsides: Firms that diversify with international projects could fare better in a downturn. But as the U.S. financial crisis fans out to Europe, Asia, and beyond, many fear that even foreign markets might not provide a reliable refuge for architects.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!