Professional Liability Insurance for Architects: When to Get Serious

The decision to buy professional liability insurance is a watershed moment for most architects and young firms. It often means that the firm has been awarded a project at a significant scale or with a significant budget, or that a client has contacted the firm with concerns about a particular project. Or it may simply mean a firm is getting serious about the future.

The majority of claims against small firms in recent years came from residential projects.

Insurance statistics: Courtesy Victor O. Schinnerer & Company

Professional liability insurance is coverage that protects an architectural firm and its employees against claims alleging negligent acts, errors, or omissions in the performance of architectural services. This is different from commercial general liability, or CGL, insurance, which covers the types of accidents or property damage that could happen at any business. CGL policies are relatively standard regardless of the type of business and usually exclude professional liability claims. In contrast, professional liability policies are as specialized and diverse as the variety of professional practices that exist.

Why firms “go bare”

According to the insurer CNA/Schinnerer, each year between 1994 and 2005 there were between 15 and 21 professional liability claims filed for every 100 firms. And yet, architects who are starting a firm on their own often don’t get insurance either because they think the risk is low on small projects, they believe their assets are so limited that they don’t have much to lose, or because their clients haven’t required it.

Strictly as a cost-benefit analysis, architects generally overestimate the costs of insurance while underappreciating the benefits. The most valuable benefit of professional liability insurance is coverage for legal costs to defend against a claim. The insurance company can provide a lawyer to help the architect gather and retain necessary documentation, and avoid taking subsequent actions that could weaken the architect’s defense. When a claim does go to trial, a small firm can be bankrupted just trying to get a dismissal. Legal assistance may be even more valuable than having coverage to pay for actual negligence.

In addition, professional liability insurers offer ongoing risk management services to insured firms. These include legal review of standard and client-provided contracts, and targeted continuing education on ways to reduce or avoid unnecessary liability.

What actions result in claims

Many young architects are surprised to learn that an architect can be held liable for the negligence of contractors and others working on a project, or that negligence claims can be based on faulty cost estimates or delays in construction. Claims can also be based on planning or feasibility studies and do not require that the architect be the architect of record for a project. And, not all clients pay their fees; it is common for an architect who brings a suit to recover fees to be subject to a counterclaim that the architect was negligent.

In general, professional liability claims are more likely to be the result of a failure to manage expectations than due to a spectacular construction failure, particularly where the client has little experience with other construction projects. Their understanding of what comprises an architect’s scope of work and the quality and timing of the final product may be unrealistic, but that does not prevent claims from being filed and even going to trial or arbitration.

An architect may be reluctant to explain delays or cost overruns to a client, hoping to “catch up” elsewhere on the project. That lack of communication may result in a bigger surprise for the client. Even where a firm has clear expertise on a certain project type, too many commitments can result in client frustration and lack of trust. These are all examples of situations that can generate professional liability claims without an obvious failure on the part of the architect to design a safe, high-quality building.

Minimizing costs

A variety of factors go into establishing the premium for a particular design firm’s policy, including the firm’s primary project type, claims history, whether they use standard written contracts, specialty coverage, and the extent of coverage required for prior acts. Project types such as condominiums, which have high litigation costs relative to design fees, or skate parks, which are unique projects with a high propensity for injuries, will typically increase the premium costs. However, documenting and reporting internal practices such as training and structured supervision of employees can demonstrate a lower risk and decrease premium costs. Although the application forms for insurance are often lengthy, completing the form accurately and thoroughly can allow the agent to more accurately assess the risk posed by a firm and justify a lower premium.

The factors in the application allow the agent to determine a fractional number or rate, which is then multiplied by a measurement of the firm’s annual billing or total project costs to quantify the annual premium in dollars. When reporting a firm’s annual fees for this calculation, architects should subtract costs such as travel or copying, or fees for work on projects that were abandoned before construction and thus do not add to liability. For new firms without a significant history of billing, the multiplier is typically a reasonable estimate of the firm’s anticipated billings for the coming year. If the premium creates a financial hardship for the firm, the agent may be able to respond creatively to an individual firm’s needs.

Nontraditional practices

Many young firms are specialized or employ a variety of innovative corporate structures and delivery methods. These can have a surprising impact on professional liability. For instance, some architects design and custom-build their projects. This is often done for small clients and allows the architects to do custom detailing on-site. However, because the professional liability of a contractor is different than that of an architect or designer, work built by the architect is not covered under the standard architect’s policy. Although many insurance companies offer a design-build endorsement for architecture policies, these only cover issues that arise from the design work done on a design-build project where the builder is a distinct entity. An architect who is personally acting as the builder would need an entirely separate design-build policy.

Although the likelihood of a claim against a firm is low (top), it’s still not unheard of.

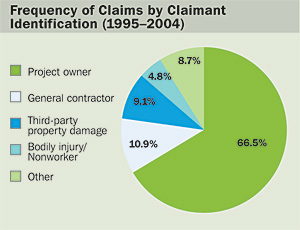

Project owners are most likely to file a claim against a firm.

Insurance statistics courtesy Victor O. Schinnerer & Company

Or say two architects team up in a joint venture to do a project. Where both parties are licensed professionals, each should have separate insurance coverage, or they may want to get a joint-venture policy specifically covering the work they do together. With a separate policy, liability for any joint projects can then be excluded from the firms’ individual policies. Where a young architect and a nonprofessional—an artist or sculptor, for example—collaborate on a project, the actions of the non-professional may be legally attributed to the architect, but not covered under the standard architect’s policy. In this case, the architect may be able to get a simple endorsement to their existing policy that adds the non-professional as a “limited insured.”

Also, architects who are not licensed often think that they cannot get professional liability insurance. This is not true. Many nonlicensed professionals, such as appraisers, building inspectors, and even social workers provide specialized services following extensive education and training, and thus seek specialized coverage. Although many insurance companies do limit their specific coverage for architects to only “licensed architects,” those companies are likely to have other policies that can cover design work that does not require a license. For instance, a nonlicensed architect doing substantial interior renovations could obtain coverage as an interior designer, or through a design-build policy if applicable. Alternatively, nonlicensed professionals who can demonstrate some basic level of experience can usually get coverage as “specialty consultants.”

Coverage in nonprofit settings

Increasingly, young architects work full-time in nonprofit settings such as community design centers. But professional liability policies covering architects are often available only to licensed architecture firms as defined by state law, and not to nonprofit corporations with just a few architects providing design services. And while it is possible that a nonprofit’s existing general liability policy could cover the organization itself for incidental professional services, the professional providing those services could still be held personally liable for any claim. One solution here is for the nonprofit to acquire what is called a “miscellaneous professional liability” policy. These policies are designed to cover people who are potentially subject to professional liability, but who work in a field that doesn’t have individualized professional liability policies. The basic miscellaneous policy is accompanied by an endorsement covering a specific profession. Although “architect” is not usually one of the professions covered in this way, the nonprofit may be able to obtain such an endorsement. Either way, it is worth noting that nonprofits often have coverage for their board members, which is also called “nonprofit professional liability.” This kind of policy should not be confused with the insurance needed by an architect who is working as a nonprofit’s employee.

Working by moonlight

Young architects who are considering starting their own business sometimes take on side projects while employed full-time. This practice is strictly prohibited by most firms, primarily in order to limit the design firm’s exposure to potential legal claims resulting from the moonlighting employee’s work. However, with careful planning and honest communication, young architects who want to engage in extracurricular activities can do so without creating liability for their primary employers. These employees should first purchase a comprehensive professional and general liability policy in their own names, and should be prepared to provide the employer with the certificate of insurance as proof (this personal policy should also have an explicit exclusion for any work done by the employee on behalf of the employer). The employee should never give an external client even the slightest impression that they are working on behalf of or supervised by their primary employer.

No work should ever be done from the employer’s office—including e-mails and phone calls. The employee should not use the firm’s business card or even a notepad with the firm’s name on it. It would also be reasonable for an employer to ask for formal certification of the above prohibitions.

Believing in the future

Architects are subject to professional liability as a direct result of the higher expectations placed on us due to our specialized education and training. Our work involves complex decisions and responsibilities—designing projects, supervising an office, observing construction, achieving client satisfaction, and ensuring the health, safety, and welfare of the public. Buying insurance is not about avoiding risk, but it is an important part of having the knowledge, the confidence, the resources, and the professionalism to take on and manage multiple risks simultaneously. Firms that take the plunge are optimistic (not merely hopeful) about the future ahead of them.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!